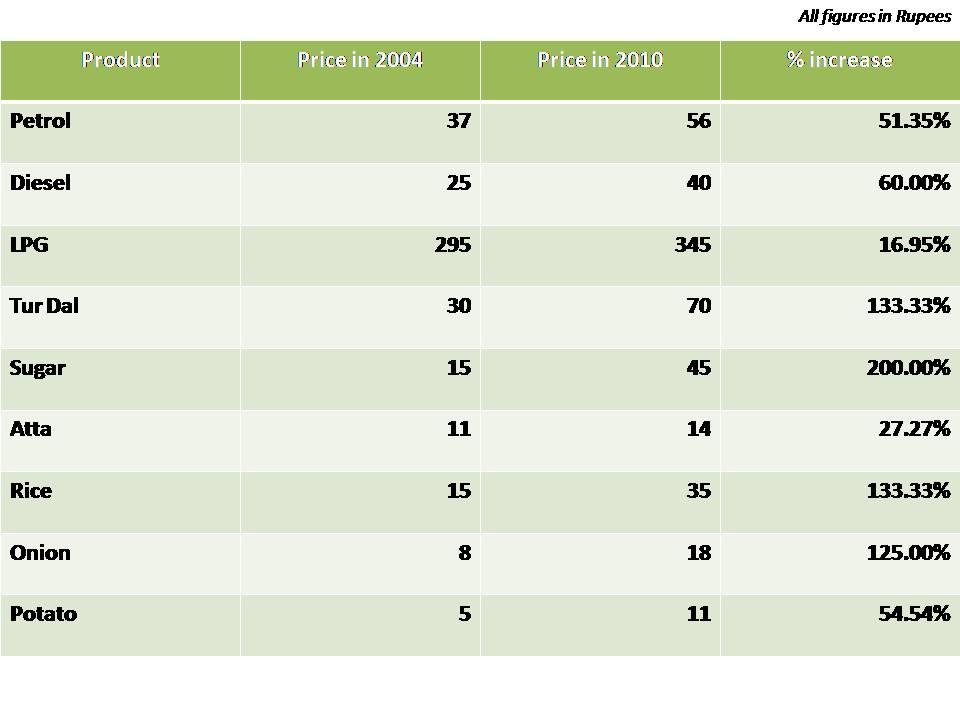

Petrol prices have risen by more than 75% since 2004. So does essential items like daal, chawal, vegetables etc. Rise in Loan EMIs in recent years have given sleepless nights to borrowers. Most of them have to relook at their finances and cut short expenses even on essential items to deal with the scenario.

How does it affect You

All of these situations are related to one factor which affects our lives immensely-Inflation. It has been riding the wave since it started rising. Most economists track it because it has a very high effect on economy. A mild inflation is always good for economy, but when it rises very high (almost out of control), it jeopardize the savings as the currency of the country gets impacted.

Cost of education, & expenses, savings, investments- all these get affected due to inflation. Hence, it becomes equally important to understand the impact and take it into consideration while planning our life goals.

What is this Inflation?

There are numerous items we consume. Sometimes a demand supply mismatch happens on these due to various reasons and price of these items rises. This rise in price is termed as inflation. Recent example is very high rise in prices of onions as there was heavy shortage. The inflation is always shown in % which indicates how much the price has risen in the index. However, it does not signify that price of every item we consume has risen.

How do we measure it

There are two ways to measure inflation:

1. WPI or Whole Sale Price Index– WPI is the index that is used to measure the change in the average price level of goods traded in wholesale market. In India this is taken as an indicator of the rate of inflation in economy.

2.CPI or Consumer price Index– CPI is a price index that tracks the prices of a specified basket of consumer goods and services, providing a measure of inflation.

In India WPI is use to track inflation but economist have been advising government to use CPI, like globally, as WPI does not reflect the correct picture since it measure price rise at wholesale level and not what the end consumer consumes. The difference can be seen in recent times when although WPI index have fallen in some years, the CPI has been rising constantly due to presence of essential items like vegetables.

Inflation directly impacts your purchasing power. An item which has cost you Rs 500 today, will be worth Rs 530 next year if inflation is 6%. Thus, if there are rise in prices, you will have to shell out more for buying same goods & services.

Looking at the charts below gives you an idea how price rise have increased year by year which has resulted in cost of essential item rising manifold.

Infact prices of essential items have increased by more than 100% when you look at longer horizon. These items are used in your household daily and form the major chunk of your expenses.

Rampant increase in prices of these daily used items affects your household budgets. However, your income never increases in the same ratio. This in turn impacts your standard of living.

Impact on Savings

Comfortable Retirement, Children’s future Planning, Buying a house, car etc. are concerns around which the life of a common man revolves. These goals form the major portion of one’s expense in their budget. As the priorities changes the ratio of a particular expense too changes. For e.g in the initial years self expense is high while in later years of life, children education expense take up more than 50% of the budget. Inflation impacts all these goals adversely. The amount of savings one need to do to meet these goals is heavily dependent on the amount of funds required for respective goals. If inflation is high, the need of funds will keep on compounding with the required number. This increases the amount of savings required and sometimes go out of reach if delayed due to various reasons.

Given below is an illustration reflecting the rise in corpus required due to inflation:

Expense | Current value Rs. | Inflation (%) | Value after 20 years Rs. |

Household | 400000 | 7 | 1547874 |

Education | 1000000 | 10 | 6727500 |

Retirement | 100000 | 7 | 672750 |

As can be seen the value of Rs 1 lakh today will be Rs 672750 after 20 years. The household expense too increases to Rs 1547874 after 20 years. This increase restricts the amount of savings you can do since income do not increase at the same rate. Hence a longer time horizon is required to reach the inflated figures with fewer amounts of savings.

The impact is more when you are running huge liabilities. Home loan,car Loan etc reduces your capacity to save. Any increase in these liabilities along with inflation gives a double blow to your savings. Hence in most cases the planning for important life goals get delayed. And when it starts the savings required reaches astonishing figures.

Goal | Funds Required Rs | Time Horizon | Monthly Savings Required Rs | Return assumed % |

Education | 6727500 | 15 yrs | 14135 | 12 |

Education | 6727500 | 8 yrs | 42843 | 12 |

As can be seen from the above table, the savings required keeps on increasing as you delay the financial goals.

Impact on returns

The returns you earn on any investments also get impacted by inflation. The net return earned on investments can be quite low when inflation is considered. For e.g. if a fixed deposit is offering interest rate of 7% and inflation is 5% the return you earn is only 2%. Add the effect of taxability you might be losing money instead of earning anything. Hence, inflation eat out returns earn on investments which impact your goal achievement.

Inflation will always be there. We cannot live without it. The only way to tackle is planning ahead. Consider inflation while planning all your future expenses. When investing for your goals aim for returns more than inflation. The early planning can help in meeting desired financial objectives with your available resources.

Post Disclaimer

IMPORTANT DISCLAIMER!

This and All the other Articles/Videos on this blog are for general Information and educational purposes and not to be taken as an Investment Advice. Any Action taken by Readers on their Personal finances after reading our articles or listening to our videos will be purely at his/her own risk, with no responsibility on the Writer and the Investment Adviser. Registration Granted by SEBI, membership of BASL and Certification from National Institute of Securities Markets (NISM) in no way guarantee performance of the intermediary or provide any assurance of returns to investors.