Rise in interest rates for last few years have open opportunities for investors in fixed income segments. Not only traditional instruments like fixed deposits, but schemes from debt mutual funds have seen a surge in interest among risk averse investors. The primary reason is the high yield due to high interest rates along with tax efficiency provided by this category.

Who should consider Dynamic Funds?

Although there are various Debt Mutual Funds scheme which an investor can select based on his time horizon and risk apetite, dynamic bond funds have been showing stellar performance in recent times. These funds have been able to capture the interest rate movement well and have been generating good returns.

Let’s understand how these funds works and when can an investor consider these in his portfolio

What are Dynamic Bond Funds?

Dynamic Bond Funds are debt Mutual funds scheme which invest across the spectrum of investment grade debentures, Certificate of Deposit, Commercial papers, Bonds and government securities. The exposure to each of these instruments vary within all schemes and is on the discretion of fund manager. Unlike general debt funds, dynamic bond funds do not have a mandate of maintaining fixed proportion in any of these instruments.

How They Work ?

In any general debt fund, investment in underline securities are kept in a fixed proportion and the maturity of these securities, which is in line with scheme objective, do not change frequently . If it’s a long term fund like gilt or income the securities in its portfolio will be of longer maturity while in a short term fund the securities will be of short duration. Since these securities are impacted by change in interest rate the fund manager may reshuffle the impacted securities (e.g. gilt in income funds) frequently. But there is no frequent change in entire portfolio.

Contrary to this in a dynamic bond fund the fund manager has flexibility to change duration of portfolios by altering the proportion of investment in various securities based on his view of interest rate movement. So if interest rates are expected to rise going ahead, fund managers lower portfolio maturity by increasing shorter-term papers in the portfolio. Short-term bonds face lower impact of interest rate hike and enable fund managers to cash in on market volatility in the shorter end of the yield curve. Current portfolios of these funds shows major holding in NCDs, CDs and commercial papers depicting shorter maturities of the portfolios. On other side if it’s a falling interest rate scenario the duration of portfolio is increased to grab the opportunity as long term bonds prices rises whenever there is fall in interest rates, producing higher returns. Thus the fund manager tries to time the market by altering the proportion of gilts and corporate bonds to generate superior returns.

The other flexibility which a fund manager has is moving into cash. The entire portfolio can be moved to cash position if interest rates are moving very sharply in short duration. This helps fund managers to avoid risk of taking wrong calls and deploy funds when there is an opportunity.

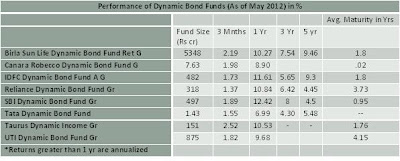

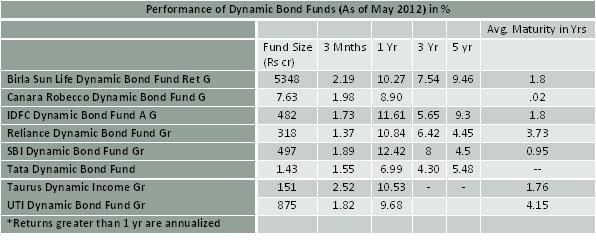

Performance

Most dynamic funds have been able to show a strong performance in recent times. The primary reason is the active management and quickly reposition of the maturity profile as per the interest rate environment. SBI Dynamic Bond Fund, which had increased its average maturity profile to an excess of eight years in November 2011, cut it to less than a year in March 2012. Reliance Dynamic Bond Fund, which had increased its average maturity to 11.5 years in November 2011, cut it to 3.73 years in March 2012. This strategy has paid off well for these two funds which have grabbed the no 1 spot in last quartile. Most other dynamic bond funds have also cut their average maturity, especially in the month of March.

If one look closely at the performance in long term then only few of the funds have been consistent .Birla Sun Life dynamic and IDFC Dynamic bond funds are two funds which have seen both market scenarios and have fared consistently in short and long term. SBI Dynamic and Reliance Dynamic bond Fund have been in top quartile this year due to effective Fund Manager calls but long term performance still lags behind. The other funds do not have a long track record and their corpus have been tilting downwards. With active management of average maturity of portfolio, dynamic bond funds are expected to generate returns in both interest rate scenarios.

There are other funds too which do not have dynamic name attached but managed by similar strategy.BNP Paribas Flexi debt, Kotak Bond Regular,Sundaram Flexible Income,L&T Select Income –Flexi debt and HDFC Medium Term Opportunities are some of them.

For retail investors it is difficult to select funds based on interest rate call and do active management. The debt market has been difficult to understand even by some financial advisors. Hence, it may be a good idea to leave the interest rate prediction to the experts i.e. fund manager. A dynamic bond fund can be a good selection to benefit from interest rate movement in both scenarios. For 3-6 months if interest rates rise dynamic bond funds are expected to produce higher returns with dip in average maturities of their portfolio. However, for a longer horizon barring Birla Dynamic Bond Fund which have Large asset base, low (although fluctuating) expense ratio, low volatility coupled with good returns and IDFC Dynamic Bond fund which has been able to manage its portfolio well, others have to still prove their mark. Investors who do not wish to take interest rate call by themselves this year can include dynamic bond funds in their portfolios. Low maturity will yield good returns in next 3-6 months if interest rates heardened.. For long term investors who are comfortable in taking a higher risk they can consider general debt funds like gilt or income which will produce higher returns in next 2-3 years when interest rates falls. Even Birla Dynamic or IDFC Dynamic fund is a good choice if one has to avoid taking interest rate call by themselves in long term and reap benefits in both interest rate scenarios. One inherent risk factor which should bear in mind is that the performance of dynamic bond funds relies solely on Fund Manager, whose track record plays a very important role here.

As Published in Business Bhaskar on 7th May,2012

Post Disclaimer

IMPORTANT DISCLAIMER!

This and All the other Articles/Videos on this blog are for general Information and educational purposes and not to be taken as an Investment Advice. Any Action taken by Readers on their Personal finances after reading our articles or listening to our videos will be purely at his/her own risk, with no responsibility on the Writer and the Investment Adviser. Registration Granted by SEBI, membership of BASL and Certification from National Institute of Securities Markets (NISM) in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

Good article on Dynamic funds.

Wondering how do they compare against the short term funds!

Bemoneyware,

Thanks…

Dynamic Bond funds will have an edge over short term when markets are in opposite direction. A short term fund does not changes its portfolio much but a dynamic bond fund do.So when interest rate start falling dynamic bond funds will allign its portfolio accordingly to reduce the impact of interest rates.A short term is strictly for a short horizon while a dynamic fund horizon can vary, some do have a long term track record also.So the difference is really static and dynamic.

mere ko kaise shuru karna chahiya.Aur kya mai abhi start kar sakta hu. mai 34 ka hu aur meri salana kamai 168000 hai. 4000 tak hi save kar sakta hu. apne parivar ke liye mujhe kya karna chahiya kuch taki 60 tak mai kuch jod pau. ek beta hai mere uske or wife ke liye

kuch karna chahta hu.

dhanywad.

Anonymous,

pehle to ek term plan le lo monthly payment par jo tumhe Rs 700-800 tak padega aur ek Health insuranvce bhi le lo. Uske baad 2000 rupee ki SIP shuru kar do mutual fund mein ye dhyan mein rakhte hue ki kab tumhe paisa chayiyeh jise bache ki padhai. 1000 p.m ki bank mein RD account khulwao agle das saal ke liye jo tumhe achi income dega aur jaroorat mein use kar sakte ho.

Sir,

I am 26 and want to save tax. Annual income is 6 lac (CTC) with some deductions. I want to save money for future plus it should also comes under rebate, what would you recommend and what are the risks?

I have already two LIC each 12K. I can invest 5k per month.

Please guide.

Sandeep,

There are various investment options for tax saving and each of them has its characteristic. PPF, ELSS, NSC, FD (Tax saving), NPS can be utilized for claiming tax benefit. But some of these instruments are very long term and help you in meeting some long term goals. Tax saving is an additional advantage available in them. My advise will be that you first identify whether you need these long-term instruments. For example if you are planning for your retirement then NPS can be considered and it will help you in tax saving. Similarly if you wish to invest for some long term accumulation then PPF can be considered. Else for medium term, say 5 years, ELSS can be chosen.

Work on these points I have spoken. It will help you in choosing the right tax saving option.